Implementation of IFRS'16 / USGAAP regulations for Leasing Contracts

Implementation of IFRS'16 / USGAAP regulations for Leasing Contracts.

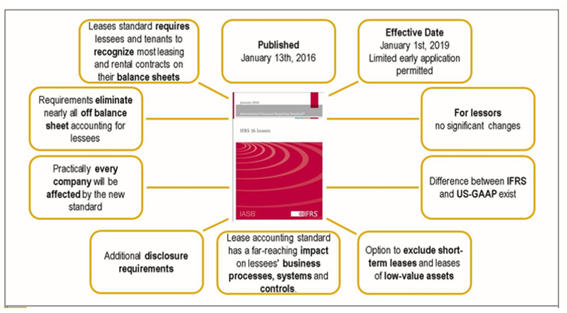

On 01.01.2019, the new accounting regulations IFRS'16 for Leasing contracts entered into force. At the same time, countries that have to account according to the regulations of US GAAP have to comply with the accounting criteria of ASC842.

This accounting requirement is not only mandatory but also has a strong impact on the financial statements of entities applying International Financial Reporting Standards.

The most significant change was in the way leases are accounted for from the lessee's perspective. IFRS 16 abolished the dual accounting model for lessees, which distinguishes between financial lease contracts (recorded on the balance sheet) and operating leases (whose future rights and obligations are not currently recognized on the balance sheet). With the introduction of IFRS 16, a single model has been developed within the balance sheet that is similar to the current finance lease.

The objective of IFRS 16 is to obtain information that faithfully represents lease transactions and provides users of financial statements with a basis for assessing the amount, timing, and uncertainty of lease cash flows. To achieve this objective, a lessee must recognize the assets and liabilities arising from a lease.

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognize assets and liabilities for all leases with a term of more than 12 months unless the underlying asset is of low value. Para cumplir con ese objetivo, un arrendatario debe reconocer los activos y pasivos derivados de un arrendamiento.

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognize assets and liabilities for all leases with a term of more than 12 months unless the underlying asset is of low value. A lessee must recognize a right-of-use asset, which represents its right to use the underlying leased asset, and a lease liability, which represents its obligation to make lease payments.

Main management tools

Option 1: Spreadsheets/ Software provided by audit companies

Initially, this approach was chosen by most companies because it provided an immediate solution to the regulations and was simple and quick to adopt. The main problem with this approach is that such tools often have the following weaknesses:

-

Does not have integration of tools with SAP

-

Are not able to manage large volumes of contracts

-

It is practically impossible to manage contract renewals and annual fee changes (due to CPI or inflation)

-

Difficulty covering the regulations of Long and Short Term Reclassification

-

No integration with the SAP Purchasing module

Option 2: SAP Standard solution

This is a solution that covers IFRS'16 and USGAAP regulations via the standard module SAP Real Estate (RE-FX).

The standard solution allows you to cover the regulations with or without integration of the Fixed Assets module. If the solution chosen by the customer is through the Fixed Assets module, this is automatically created for the contracts to reflect the right of use of the contracts in the Balance Sheet.

Nevertheless, it has a number of disadvantages that make its cost very high compared to other solutions. We highlight these:

-

Mandatory requirement for the activation of a high Enhancement Package level

-

A mandatory prerequisite for the activation of the Business Function EA-FIN

-

A mandatory prerequisite for the activation of the module SAP RE-FX and the license

The inconveniences reflected in the first solution do not exist when implementing the SAP standard.

The average implementation time of the solution is usually about 6 months and the solution is also compatible with customers on S/4HANA.

Option 3: CUVIV product solution

Like CUVIV's standard solution SAP, it enables coverage of both IFRS'16 and USGAAP regulations.

As it is an ABAP Add-on within the CUVIV engine, it has full integration with the SAP system and also enables integration with the Fixed Assets module.

Unlike the standard solution SAP, which is managed by the module SAP RE-FX, our product has none of the 3 limitations reflected by the standard SAP. It can be implemented without activating the Business Function EA-FIN in any SAP ECC and S/4HANA system (regardless of version) and does not require activation of the RE-FX module (or its licensing).

The disadvantages of the first solution do not exist when implementing our product.

The project usually takes about 3 months and is usually cheaper than the standard solution.

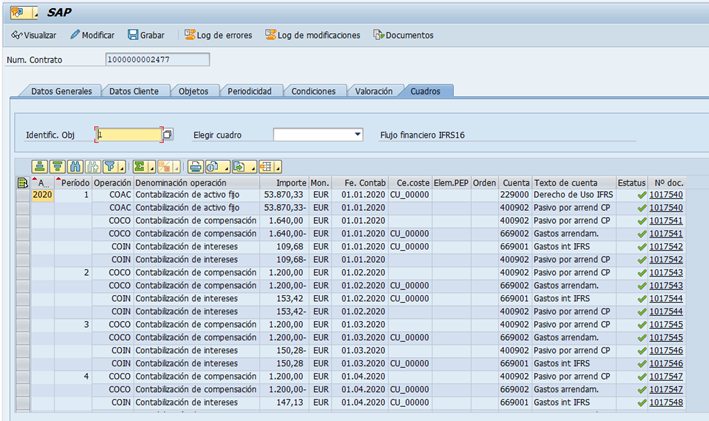

Below you can see an example of the IFRS'16 valuation and the derived accounting flows: